- Investing

While this phenomenon seems counterintuitive, it would make sense if investors operate with the assumption that central banks will continue hiking interest rates without limit no matter how high inflation gets in order to bring it back down to their targets. In reality, how true is this assumption?

Recently, there has been an interesting correlation repeatedly occurring in the markets. Whenever reported inflation figures pose a surprise on the upside, any assets that typically protect from inflation such as property, commodities, equities are being sold off.

As I discussed on Bloomberg last week, central banks may be more limited in their inflation fighting ability than generally assumed by the investing public, for the following reasons:

1. Economic risks. Central banks may say that the potential risk of causing a recession is acceptable to bring down inflation. But ultimately public pressure and concern about overall financial markets stability might prompt them to soften, if needed.

2. Hiking interest rates alone might not work to bring inflation back in line (it can soften demand for non-essentials for a while, but won’t bring about more supply of commodities etc., in fact, it could dent investment in production as well).

3. Government with high deficits may need inflation and negative real interest rates to keep debt levels sustainable. The second and third points have often been seen as controversial – however, just last month, the Federal Reserve Bank had published a report Inflation as a Fiscal Limit1 confirming these points, stating:

"Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilised by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances […] inflation will rise to ensure sustainability of national debt.”

Does it sound almost as if the Fed is pre-emptively shifting the blame for a potential future loss of inflation control onto the government?

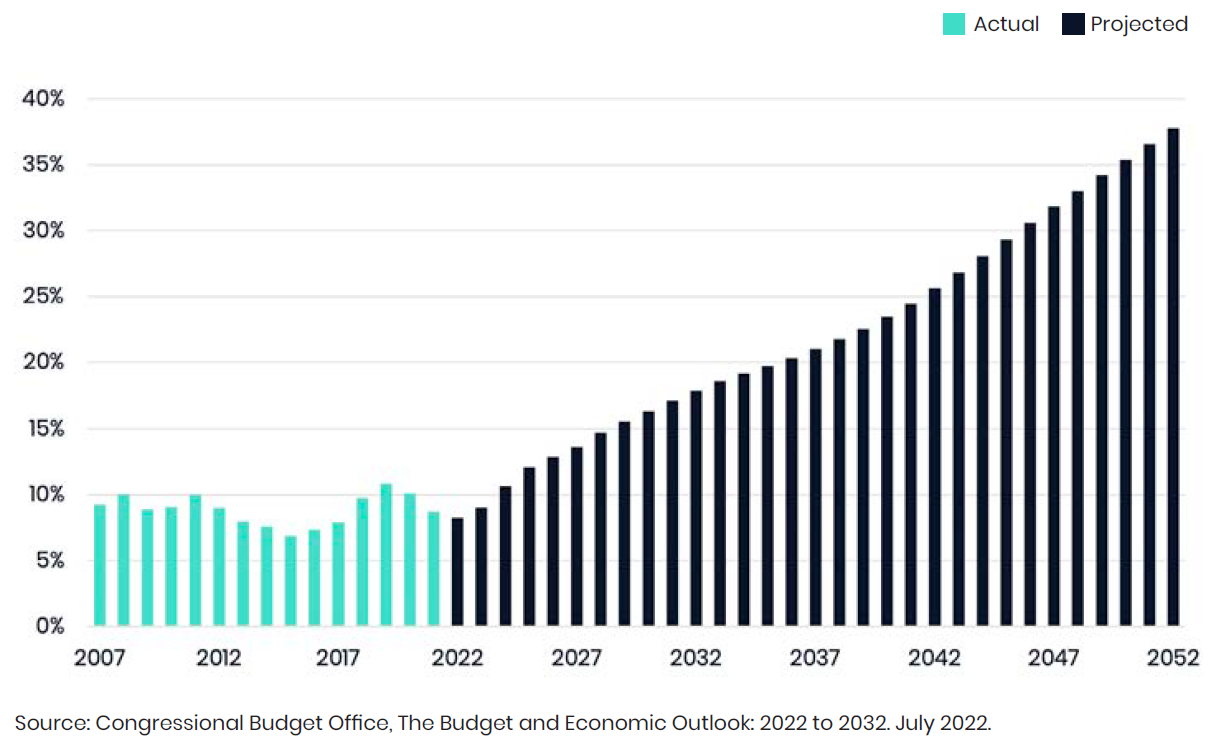

In June 2022, the Congressional Budget Office (CBO) has projected budget deficits at an average annual shortfall of $1.6 trillion from 2023 to 2032. Furthermore, they have also estimated that over the coming 30 years interest payments will total $66 trillion, as approximately 40% of the US total government revenues, would have to be allocated to interest payments alone by 20522. In any case, that would seem that further hikes might not have a much higher ceiling than current market expectations.

Investor sentiment remains poor, while attractive valuations can be found in many places. There are still risks in the global economy, which will always be present in times of general pessimism. However, we should not forget that markets are always anticipatory by nature. Historically, some of the best investment opportunities often coincide with greatest broad-based investor pessimism.

In fact, a historical analysis of over a 100 years of stock markets actually reveals a surprising negative correlation between economic growth and stock market returns.

I was recently asked by RTHK and AsianInvestor about China’s economy along with the risks that deglobalisation may bring to the region. The implementation of the world’s largest free trade zone – the Regional Comprehensive Economic Partnership (RCEP) – is gathering momentum this year, with Indonesia ratifying the pact earlier last month. For investors with a higher volatility tolerance, the recent weakness in Asian asset prices (including from a currency perspective) does imply opportunities in our view. Looking at the potential ceiling on future US rate hikes due to debt constraints, this could lead to a pause if not reversal of USD strength as well. As always, we highly recommend being positioned in well-diversified global portfolios, as no single asset or market is risk-free, with many uncertainties from economics to geopolitics remaining even as COVID-19 appears to be fading at long last.

This article is provided for informational purposes only. It should not be relied upon as financial advice and it does not constitute a recommendation, an offer or solicitation. No responsibility can be accepted for any loss arising from action taken or refrained from based on this publication. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted.

The value of an investment will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

An investment in equities and shares will not provide the security of capital associated with a deposit account with a bank or building society.

Source

1. https://www.kansascityfed.org/Jackson%20Hole/documents/9037/JH_Paper_Bi…

2.https://www.pgpf.org/blog/2022/05/interest-costs-on-the-national-debt-set-to-reachhistoric-highs-in-the-next-decade

Most popular articles

Most recent articles