- News

- Investing

Welcome to the latest issue of our quarterly CIO insights.

At a glance

- Momentum has dominated markets over the past year, but an increasingly small group of companies is responsible for a growing share of performance.

- AI continues to drive innovation and earnings growth, but elevated valuations and record levels of investment are raising the stakes - future returns will need to justify increasingly ambitious expectations.

- Winning matches is not the same as winning tournaments - successful investing requires resilience, discipline and diversification as well as momentum.

This summer has given us the biggest World Cup in history, with 48 teams and three host countries. Growing up in England, World Cups were the defining rhythm of summer – fleeting sunshine, long daylight hours, and the uniquely British ritual of crowding into pub gardens with friends and strangers alike to ride the highs and lows of England's fortunes. So, I’ve found myself staying up to watch the games despite the time zone challenges.

One of the things I find most curious about tournaments is how quickly fortunes can change. A giant (like Brazil) can look invincible, only to be humbled by a hungrier, more agile challenger. Meanwhile, an unfancied outsider such as Cape Verde can quietly disrupt the established order and force the defending champions into extra time. Expectations shift, narratives evolve, and yesterday's form quickly becomes old news.

Markets are no different. Leadership shifts and yesterday’s winners rarely stay on top indefinitely. Markets are currently rewarding ‘momentum’ – that is, stocks that have been outperforming recently – the portfolios that endure are unlikely to be those that simply chase what has worked most recently.

Yet building a successful portfolio, like building a successful tournament team, is about more than backing whoever happens to be leading today. The challenge is to build for the whole tournament - having enough exposure to capture opportunities, but enough diversification, valuation discipline and resilience to cope when leadership changes.

The uncomfortable truth, in football and in investing, is that past performance can tell you how a team got here, but not necessarily how far it can go from here. Past performance is no guarantee of continued future success.

Mind the gap: quality in a momentum-driven market

One of the most striking features of the current environment is the growing divergence between different investment styles. The gap between momentum, value and quality has widened materially over the past year.

As in football, where recent winners often carry momentum into the next match, markets can show similar patterns.

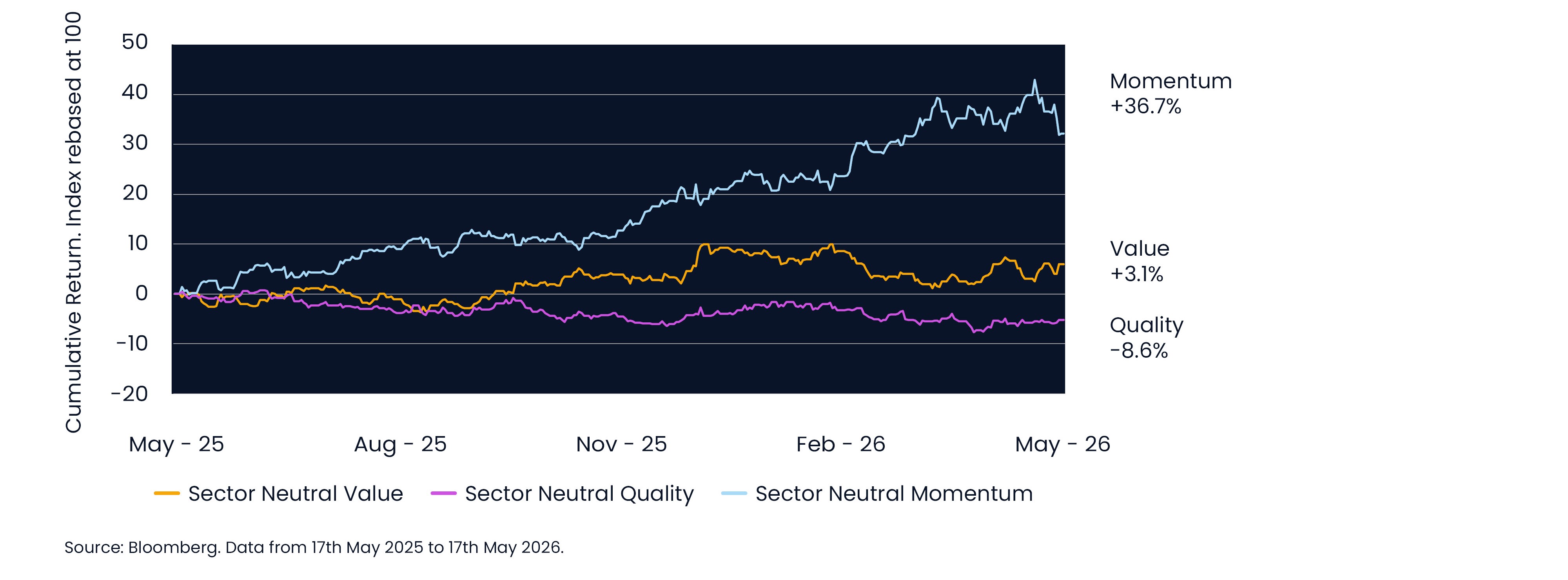

The chart below illustrates three styles: Momentum, Value and Quality. Momentum reflects recent market winners, quality focuses on resilient earnings, and value on lower valuations and more modest expectations.

Over the last 12 months, momentum has delivered strong and sustained outperformance, while value has remained relatively flat and quality has lagged.

What stands out today is the scale of the gap. Momentum is now around 45 percent ahead of quality over the past 12 months, creating a much wider spread between winners and losers.

We know that different styles move in and out of favour over time – that is not new. What matters is the extent to which the divergence is now shaping overall outcomes. A relatively small group of companies are driving a disproportionate share of returns, often supported by strong sentiment and increasingly crowded capital flows.

This divergence is not just limited to styles. We have also seen shifts in regional leadership. For a period earlier this year, the US took a back seat, lagging the rest of the world as market leadership broadened. Emerging markets, in particular, have delivered strong returns, outperforming global equities by a meaningful margin. The lesson here is that leadership changes. When it does, portfolios that rely too heavily on one source of return can become more vulnerable than investors may realise.

AI, concentration and capital flows

The drivers of this increasingly uneven market can be seen most clearly within some of its dominant themes. AI is probably the clearest example of this tournament dynamic. A small number of exceptional players are carrying a large part of the market, while the rest of the squad is still being judged on whether it can prove its role in the system.

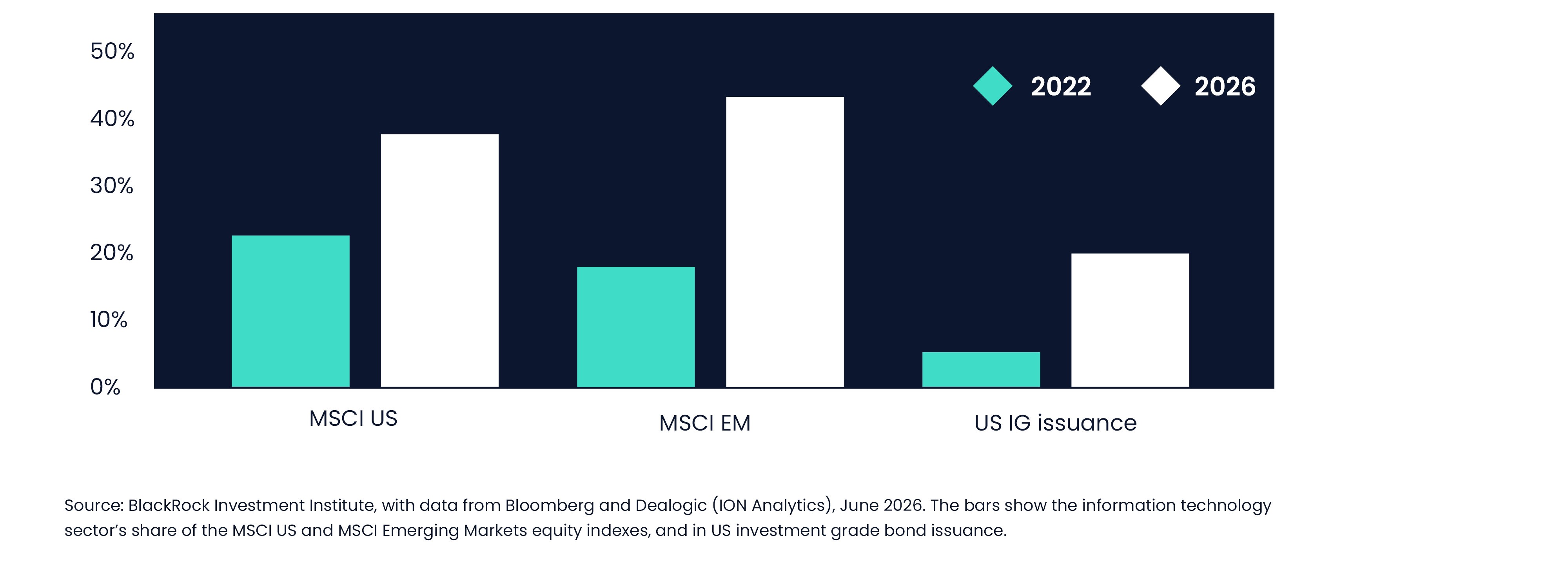

This growing influence is visible at a broader market level. Exposure to technology and AI-related sectors has increased significantly across both developed and emerging markets, as the below chart shows.

But it is not a single, uniform story. Outcomes have diverged significantly even within the AI theme itself.

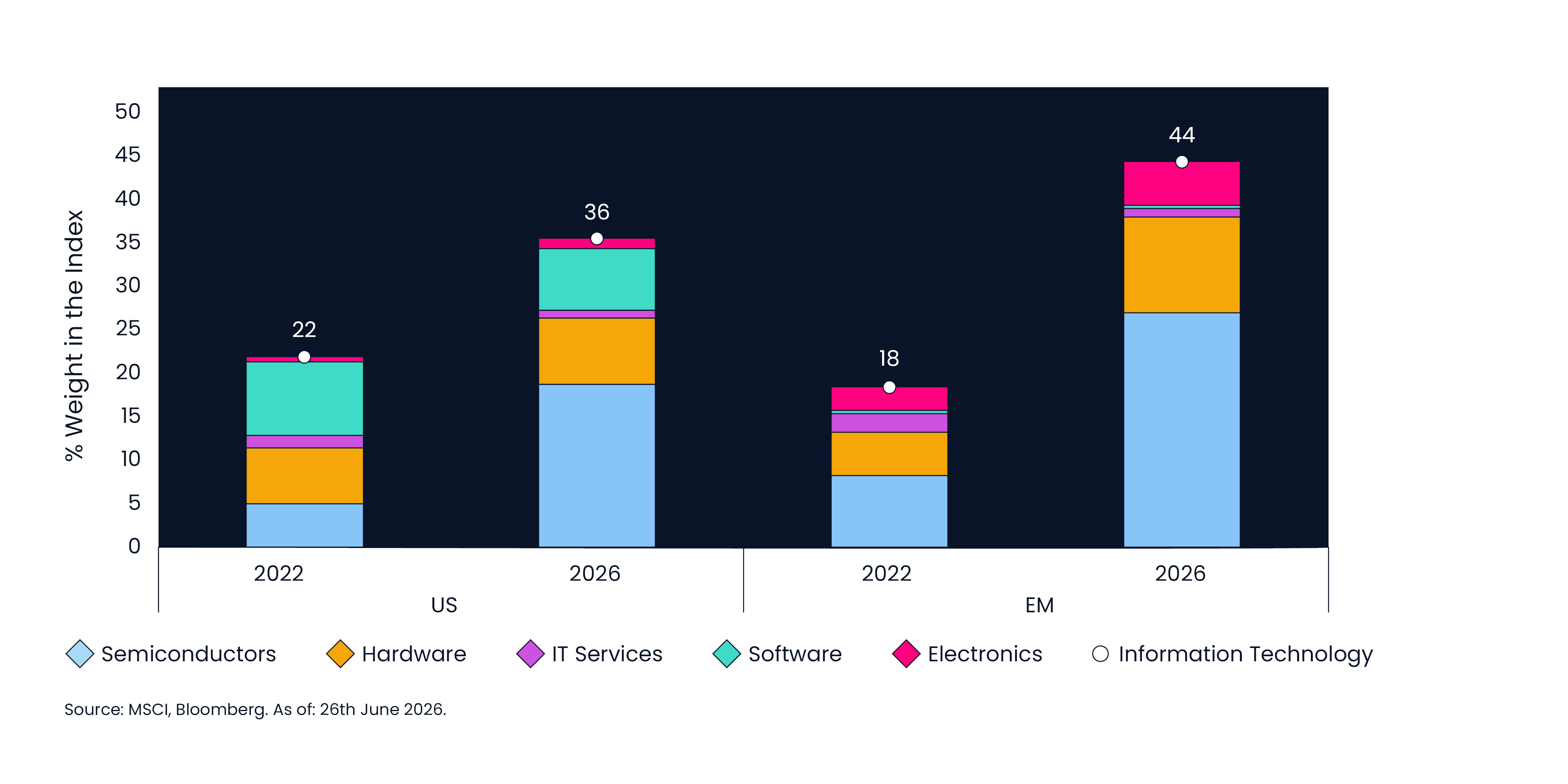

Companies exposed to the infrastructure build out – including semiconductors, data centres and parts of the energy complex – have seen strong earnings momentum and sustained investor demand. By contrast, other areas, particularly within software, are facing a more uncertain path, where the timing and scale of monetisation remain less clear. The chart below shows the overall weight in the index of the IT sector (the yellow dot), and the sub sectors that make up the total.

The risk is that markets appear diversified at the index level, while returns are increasingly driven by a narrow group of companies.

New players, crowded pitch

This concentration is also being reinforced by a new dynamic. The pipeline of large, AI-related listings is beginning to build, with a small number of high-profile companies attracting or expected to attract significant investor demand.

This next wave of listings may broaden the opportunity set, but it could also reinforce the concentration if money continues to flow to a relatively small group of names, increasing risk.

Taken together, this creates a more complex environment. Innovation and earnings momentum remain strong, but they sit alongside rising concentration, elevated expectations and increasingly flow-driven outcomes, reinforcing the need for a selective and disciplined investment approach.

Avoiding the early exit

When short-term returns are concentrated and momentum driven, the temptation is to extrapolate what has worked most recently. But the conditions that have driven recent performance, including narrow leadership, strong sentiment and crowded flows, are not always the most reliable guide to longer-term outcomes.

This is particularly true when expectations are already elevated. Across markets, there are areas where valuations leave less room for disappointment.

This creates a more uneven investment landscape. Outcomes depend increasingly on positioning, and short-term performance can diverge significantly from longer-term fundamentals.

The sensible medium-term approach is not to ignore momentum – but nor to chase it blindly. The discipline is in recognising what has worked, asking what is already reflected in the price and being clear-eyed about where risks are building.

That means focusing on valuation – buying more attractively priced assets, maintaining diversification discipline and being selective in what we hold.

We cannot predict how market leadership will evolve from here. But we can control how we prepare for it. In a market of extremes, avoiding unforced errors becomes just as important as capturing opportunities.

Final thoughts – Build for the whole tournament

Momentum can carry a team through the early rounds. However, the best teams are not always those that start fastest. They are the ones with discipline, balance, squad depth and the ability to adapt when the game changes.

That is how we should think about portfolios today. In a market shaped by momentum, concentration and crowded flows, the temptation is to chase winners. But the real challenge is to build portfolios that can last the whole tournament.

That means staying focused on fundamentals, valuation, diversification and resilience – and avoiding the mistake of confusing short-term form with long-term strength.

The timing of any shift in market leadership is uncertain. Being prepared for it is not.

Disclaimers:

Please note that past performance is not indicative of future performance, and the value of an investment with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

This article is a general communication that is provided for informational purposes only. It should not be relied upon as financial advice, and it does not constitute a recommendation, an offer or solicitation. No responsibility can be accepted for any loss arising from action taken or refrained from based on this publication. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted.

Most popular articles

Most recent articles